Is the US Mobile Industry Competitive?

5 Nov. 2017

By: Jeff Hannah

Plotting the Proposed Merger Between T-Mobile and Sprint Along the Industry Consolidation Curve

The enactment and enforcement of antitrust law within the United States has been closely aligned with each Industrial Revolution. Beginning with the First Industrial Revolution in the early 1800s, which formed industrial titans in the railroad, iron and chemical industries, led to the enactment of the Sherman Act in 1890. The intent of the Sherman Act was not to prevent competition, but rather protect the public from market failures, thus Sherman Act enforced the ex post, or after the fact, breakup of several industry leaders, most notably the breakup of the Standard Oil Company.

With the Second Industrial Revolution, which comprised of industrial and technological innovations such as the telephone and the automobile, revisions to the Sherman Act were enacted, resulting in the Clayton Act of 1914. With the Clayton Act, the Federal Trade Commission (FTC) and Department of Justice (DOJ) – the US’s lead regulators for commerce and antitrust review – became empowered with ex ante, or preventative, review of mergers and acquisitions perceived to be anti-competitive or monopolistic and thus could harm a certain industry’s market competition. Both the Sherman Act and the Clayton Act were the impetus to US Attorney General filing suit against AT&T Bell in 1978 and the eventual breakup of the regional AT&T Bell operating companies in 1984. Today, these Acts continue to be used as justification for regulatory oversight as two of the US’s largest mobile network operators, Sprint and T-Mobile, seek to merge.

But whether competition exists in today’s mobile industry remains an unanswered question. In September 2017, the FCC released its 20th Annual Report and Analysis of Competitive Market Conditions with Respect to Mobile Wireless, Including Commercial Mobile Services, which concluded that “there is effective competition in the market place for mobile wireless services” despite party-line dissent amongst FCC commissioners and documented consumer frustration with the quality and coverage of mobile wireless services. Mobile wireless communications services are the product of today’s current industrial revolution – the Third Industrial Revolution – and one may argue that the global economy is verging on the Fourth Industrial Revolution with the advent of ubiquitous mobile connectivity, cloud computing, data analytics and automation. As the US mobile industry closes on the Third Industrial Revolution and embarks on the Fourth Industrial Revolution, evaluating the state of competition – and whether to hinder or accept further consolidation of US mobile network operators – will influence early winners and losers as the US and the broader global economy enters the Fourth Industrial Revolution.

The formation of each industrial revolution and subsequent consolidation of industry players has followed a predictable S curve. A 2002 article published within Harvard Business Review on the book Winning the Merger Endgame: A Playbook for Profiting from Industry Consolidation highlights the predictably of mergers and acquisitions – and the ultimate end-game for corporations. Written by Stefan Zeisel, a consultant analyst at A.T. Kearny, a global consulting firm with focus on multiple industry sectors, the book provides a “long-term analysis of mergers around the globe [and] has found that most industries progress predictably through a clear consolidation life cycle – and that companies can plot with some precision where they fall in the cycle.”

Following the four stages of the Consolidation Curve outlined by Zeisel, the book’s premise provides valuable insight into the state of competition of the US mobile communications industry, but also an understanding of what regulators may expect with respect to the impacts of consolidation – or lack thereof – in the mobile communications industry. By comparing the Consolidation Curve stages to the historical, current and future progression of the mobile communications industry, US regulators may be better equipped to determine if there is in fact competition within the market, access the chess moves being made by mobile network operators today as they either evolve or go extinct with the advent of the Fourth Industrial Revolution, and ultimately, whether or not further consolidation, namely the merger between Sprint and T-Mobile, is beneficial or harmful to the US mobile wireless services industry.

Stage One: Opening

Zeisel’s describes the first stage along the Consolidation Curve as beginning “with a single start-up or with a monopoly just emerging from a newly deregulated or privatized industry.” With the 1984 breakup of AT&T Bell operating companies, the wireline telecommunications industry went from a government sanctioned monopoly comprised of regionally-based Bell operating companies (RBOCs) to an industry comprised of disaggregated privately-held providers offering both traditional wireline telecommunications services as well as new, higher revenue generating advanced communication information services, which is exactly what the US’s first wireless network operator, Allied Telephone Company (Alltel), was classified and regulated as when it was formed in 1985. The next two years saw the emergence of the first three wireless telecommunications providers with the formation of two additional entrants, McCaw Cellular in 1986 and Fleetcall in 1987.

During the first stage, Zeisel notes that it is important for companies to “aggressively defend their first-mover advantage by building scale, creating a global footprint, and establishing barriers to entry by protecting proprietary technology or ideas.” For the wireless telecommunication industry this first-mover advantage was solidified by the FCC’s allocation of exclusive use spectrum licenses for mobile communications via a lottery system rather than the auction-based allocations that the FCC currently uses. As the first entrants in the wireless telecommunications industry, Alltel and McCaw Cellular were awarded or amassed via license acquisitions the first Cellular spectrum bands (850 – 990 MHz), which AT&T and Verizon Wireless currently hold 44.5% and 44.7% of respectively. Evaluating stage two of the Consolidation Curve details how AT&T and Verizon Wireless came to secure 89.2% of the spectrum first allocated by the FCC for wireless telecommunications services.

Stage Two: Scale

Stage two of the Consolidation Curve is “all about building scale. Major players begin to emerge, buying up competitors and forming empires”, according to Zeisel. Between 1993 and 1994 the wireless telecommunications industry begins to form some of the household names consumers know today: Sprint-Nextel, formed in 1993 with the acquisition of Fleetcall, and AT&T/AT&T Wireless, formed in 1994 with AT&T’s acquisition of McCaw Cellular. Shortly after the formation of Sprint-Nextel and AT&T, new entrants in the wireless telecommunications industry also emerged, including the Western Wireless Corporation and Airtouch Wireless, both of which were formed in 1994, and Bell Atlantic Mobile, formed in 1995.

Over the next ten years the wireless telecommunications industry materializes around the second stage of the Consolidation Curve. In 1999, Voicestream was launched as a spin-off from Western Wireless, but only a year later Voicestream was acquired by Deutsche Telekom and by 2001 another household name for wireless telecommunications services emerged with the formation of T-Mobile. Additionally, in the year 2000, Verizon Wireless emerged with the merger between Western Wireless and Bell Atlantic Mobile.

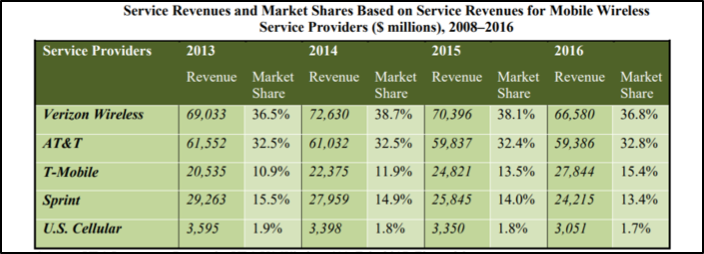

Within stage two of the Consolidation Curve, Zeisel notes that “the top three players in a stage 2 industry will own 15% to 45% of their market, as the industry consolidates rapidly.” With four major mobile network operators (AT&T, Verizon, T-Mobile, and Sprint) solidified by 2005, the next ten years followed the Consolidation Curve predictably. By 2016, the market share for each of the four

Within stage two of the Consolidation Curve, Zeisel notes that “the top three players in a stage 2 industry will own 15% to 45% of their market, as the industry consolidates rapidly.” With four major mobile network operators (AT&T, Verizon, T-Mobile, and Sprint) solidified by 2005, the next ten years followed the Consolidation Curve predictably. By 2016, the market share for each of the four wireless telecommunications operators in the US consisted of Verizon Wireless with 36.8%, AT&T with 32.8%, T-Mobile with 15.4%, and Sprint with 13.4% according to the FCC’s 2017 Annual Report and Analysis.

Stage Three: Focus

According to Zeisel, “After the ferocious consolidation of stage 2, stage 3 companies focus on expanding their core business and continuing to aggressively outgrow the competition.” It may be argued that the wireless telecommunications currently resides in the third stage of the Consolidation Curve as the four largest mobile network operators continue to hone their core business and growth plans via the acquisition of new spectrum licenses, expanded coverage maps, technological transformation, i.e., migrating from CDMA/GSM radio access technologies to LTE and the emergence of IP-based mobile broadband services.

As the mobile communications industry currently resides in the third stage, securing additional market share via Additional Revenue Per Unit/User (ARPU) has been the metric for success. However, it is important to note that in at the time Zeisel published Winning the Merger Endgame in 2002, the author placed the telecommunications industry within stage one of the Consolidation Curve. Clearly, in years after the book was published the telecommunications industry, specifically the wireless telecommunications industry, exhibited the principles of second stage. There are, however, elements to the first stage that continue to be exhibited by the wireless telecommunication industry today, namely that “companies should focus more on revenue than profit, working to amass market share” or in the case of wireless telecommunications, ARPU. This is a detriment to the wireless telecommunications industry currently and proposes a rationale for further consolidation in the US mobile communications market.

Within the CTIA Wireless Industry Indices Year-End 2016 report, between 1994 and 2016 the wireless telecommunications industry has experienced linear growth in reported subscribers, which is now calculated at 396 million subscribers. In this same timeframe, however, ARPU has consistently declined. ARPU estimates for the four largest mobile network operators averaged $34.98 as of Q4 2016 - nearly half of the ARPU collected by providers in 1994. This is good for consumers, but does not equate to a sustainable business model. There are several reasons for why the mobile communications market has seen declining ARPU. According to the FCC’s 20th Annual Report and Analysis, “new pricing plans, equipment promotions, Early Termination Fee payoffs, free international roaming, and changes in the pricing of video” are among the various promotional offers and concessions currently made by mobile network operators – all of which have been implemented by providers to capture greater market share. As Zeisel notes, within stage one “companies should focus more on revenue than profit, working to amass market share”, however, this is where the current problem for mobile network providers may reside, which is impacting consumers, regulators, and even enterprises.

In the first quarter of 2013 total postpaid subscribers equaled 217,887,000 and by fourth quarter 2016 total postpaid subscribers equaled 257,158,000, an increase of 3,927,100 subscriber lines – or a 16.5% increase – over a three-year period. There are an estimated 326,625,791 people within the US. Factoring in the number of pre-paid subscribers (77,216,000) and wholesale (25,031,000), there are currently 359,405,000 subscriber connections in the US, or more subscriber connections than there are individuals. Mobile communications supply has exceeded individual consumer demand within the US, leaving coverage and new revenue generating services associated with the Fourth Industrial Revolution as the only avenues for mobile network operators to generate organic growth in the US.

The combined market share of a merged T-Mobile and Sprint operator would total 28.4%. With Verizon Wireless holding 36.8%, AT&T holding 32.8%, and a consolidated T-Mobile/Sprint operator holding 28.4% a set of the “top three players” would emerge with “15% to 45%” of market share – the needed amassment of market share that Zeisel identifies as indicative of the second stage of the Consolidation Curve. The proposed merger between T-Mobile and Sprint would off-set the current trend, where price wars are stifling network investment and mobile network operators declining revenue, in a number of ways.

For one, a merger between T-Mobile and Sprint would assist regulators’ interests in providing adequate mobile network coverage in rural areas and increased capacity in urban areas. Both Sprint and T-Mobile hold portfolios of high-band, mid-band and low-band spectrum, but unless they are combined their assets are not mutually beneficial. T-Mobile has made several acquisitions of low-band spectrum in recent years with the acquisition of licenses in the 600 MHz and 700 MHz range, bolstering the operator’s ability to provide a wider coverage radius from a single access point. Factoring in T-Mobile’s mid-band AWS-1 (1.7 - 2.1 GHz) licenses, T-Mobile’s spectrum licenses would complement Sprint’s high-band BRS (2.5 GHz) and mid-band PCS (1.9 GHz) spectrum licenses, providing parity to AT&T and Verizon’s sizeable licenses across the low-band, mid-band and high-band spectrum blocks.

An October 2, 2017 FierceWireless article in which Andrew Miceli, vice president of global sales and marketing at Mosaik states that, “There’s no doubt this merger can significantly improve their competitive position in previously coverage-limited rural areas.” By combining needed low-band spectrum for rural coverage while bolstering the merged operator’s ability to provide high capacity mobile communications services in urban areas via high-band spectrum licenses, a merger between T-Mobile and Sprint serves both regulator as well as consumer interests. Regulators would be satisfied as rural communities would be served by improved coverage since T-Mobile’s low-band spectrum would enable greater coverage in rural areas. Additionally, consumer interest would be satisfied as consumers would be offered greater consumer choice for mobile services in terms of quality of service (QoS) and quality of experience (QoE) as the merged operator would be better positioned to provide comparable coverage and capacity, as compared to AT&T and Verizon Wireless, in both rural as well as urban America.

The second reason why a merger between T-Mobile and Sprint would benefit the US mobility market has to do with the mobile industry enabling the Fourth Industrial Revolution. AT&T and Verizon Wireless have already embarked on focusing their business model and growth strategies per the third stage of the Consolidation Curve, however, not by increasing traditional, i.e. human, market share but by focusing on new subscriber market share derived from digital convergence with various industries, such as automotive and agriculture.

According to Chetan Sharma Consulting’s US Mobile Market Update – Q3 2017 report, “IoT and Cars accounted for 62% of the net-adds” in the third quarter of 2017. This “4th Wave ecosystem is expected to grow by 60% in revenues” as IoT and Machine-to-Machine (M2M) connections become the new land grab for mobile network operators. Given their sizeable existing market share and existing network footprints, AT&T and Verizon Wireless are leading the US wireless industry in terms of delivering the connectivity needed for the Fourth Industrial Revolution, whereby the physical and digital worlds are combined. Emphasizing AT&T and Verizon Wireless’ growth on the eve of the Fourth Industrial Revolution, the US Mobile Market Update – Q3 2017 report states that “Verizon continued its steady march on the IoT/Telematics front… it is marching towards a $1B business in 2018.” Additionally, via AT&T’s agreements with automotive manufacturers, such as General Motors, AT&T “led in connected car net-adds and is a global leader in the segment.” These figures, and the new market segment consisting of things align with the FCC’s 2017 Annual Report and Analysis totals for “Connected Devices”, which grew from 2,823,300 in 4Q 2013 to 5,727,900 in Q4 2016. That’s a 67% increase over three years – considerable growth compared to the numbers for traditional prepaid and postpaid customer acquisition (16.5%).

With the bottom two mobile network operators by market share, Sprint and T-Mobile, fighting for APRU and revenue generated by a finite number of traditional subscribers, hoping to surpass 20% market share threshold by consuming subscribers from their competitors (something that T-Mobile has been able to recently achieve, namely due to the introduction of unlimited data plans, at the expense of Sprint, AT&T and Verizon), leaves the two providers in the undesirable position of being left in the flux of the Consolidation Curve’s second stage. Here, Sprint and T-Mobile are left to focus on amassing market share by making concessions that marginally increase their market share at the sacrifice of profitability. This sandbags the entire mobile communications industries’ ability to grow.

However, while Sprint and T-Mobile are left in this second stage flux, AT&T and Verizon Wireless, due to their sizeable existing market shares, spectrum portfolios, and increased revenues are able to evolve along the Consolidation Curve towards third stage, a point that Zeisel identifies as when companies should “emphasize their core capabilities, focus on profitability, and… attack underperformers”.

Stage Four: Balance and Alliance

Along the Consolidation Curve, this is where “the titans of industry reign” according to Zeisel and “industry concentration rate plateaus… the top three companies claim as much as 70% to 90% of the market. Large companies may form alliances with their peers because growth is now more challenging” (Hint: AT&T and General Motors). It is here where regulatory intervention, whether ex ante or ex post, is needed as monopolies, or even duopolies, may form. For companies to maintain their presence in the fourth stage, companies “must be alert to the potential for industry regulation and the danger of being lulled into complacency by their own dominance.”

Conclusion: Why the US Mobile Industry Should Continue to Climb Along the Consolidation Curve

The application of principles outlined by Zeisel’s Consolidation Curve provide valuable insight into the state of competition of the mobility market and the potential upsides to industry consolidation. While US regulators first eluded to blocking a merger between Sprint and T-Mobile in 2014, such a decision by US regulators, and any future dissent, may present more harm than benefit to the US mobility market. Currently, Sprint and T-Mobile are in a race to the bottom, cycling within the second stage of the Consolidation Curve with no upward mobility. Declining ARPU, declining revenue per megabyte, a finite number of traditional subscribers, and increasing CAPEX attributed to spectrum license acquisitions and network infrastructure densification are all impacting the four largest mobile network operators.

However, due to their sizeable market shares and broad spectrum portfolios, AT&T and Verizon Wireless have been able to transition to the third – and may even fourth – stage of the Consolidation Curve. A merger between T-Mobile and Sprint would place the united operators on equal footing with AT&T and Verizon Wireless in terms of market share, spectrum assets, and the ability to focus on their core business and growth plans. While a triad of mobile network operators with national footprints would be detrimental to regional mobile network operators, such as U.S. Cellular and LEAP Wireless, the alternative is the emergence of two leading mobility providers who will eventually emerge as fourth stage industry titans with little competition but each other – the classic example of a duopoly. The DOJ and FTC should take note of the predictability of corporate consolidations along the Consolidation Curve and understand that as industries mature, they inventively consolidate. The role of the DOJ and FTC should then not be to split a wedge between two high-market share providers and two low-market share providers, but rather create an industry climate of equal market share.